TABLE OF CONTENTS

Table of Contents

How to Check Your Credit Score for Free in the UK (2026)?

Nobody thinks about their credit score until the exact moment they need it to be good. Maybe you’ve just been turned down for a credit card you were fairly confident about. Maybe a mortgage broker has casually mentioned you should “sort your file out” before you start house-hunting. Or maybe you’ve simply never checked and you’d quite like to stop guessing. Whatever’s brought you here, here’s the bit that surprises a lot of people: you can check your credit score for free UK-wide, today, without paying a subscription or handing over your card details to anyone.

Thank you for reading this post, don't forget to subscribe!That’s worth saying plainly, because there’s a persistent myth that credit checking costs money. It doesn’t have to — and in 2026, it genuinely shouldn’t. This guide walks through how the UK’s credit scoring system actually works, which free services are worth your time, how to read what they show you, and what’s sensible to do once you’ve seen the number. No scare tactics, no upselling — just a clear route from “I’ve no idea where I stand” to “I know exactly what’s on my file.”

Why Bother Checking Your Credit Score in the First Place?

It’s a fair question. If you’re not applying for anything right now, why does it matter?

How to Check Your Credit Score for Free in the UK (2026)?

A few reasons, and they’re more practical than dramatic:

- You catch errors before they cost you. Credit files are compiled from data sent in by banks, lenders, and local authorities. Mistakes happen — an account that isn’t yours, a payment wrongly marked as late, an address mix-up with someone who used to live at your old flat. None of that gets fixed if nobody’s looking.

- You spot fraud early. If someone’s opened an account in your name, your credit report is usually where it shows up first.

- You avoid wasted applications. Every formal credit application leaves a mark on your file. Checking your eligibility odds beforehand, using your own free score, means fewer pointless applications and fewer unnecessary searches.

- You can plan ahead of a mortgage or car finance deal. Lenders look back over months, sometimes years, of behaviour. Three months’ notice to fix something is far better than finding out at the worst possible moment.

None of this requires a paid subscription. It requires about ten minutes and one of the free services below.

How UK Credit Scoring Actually Works?

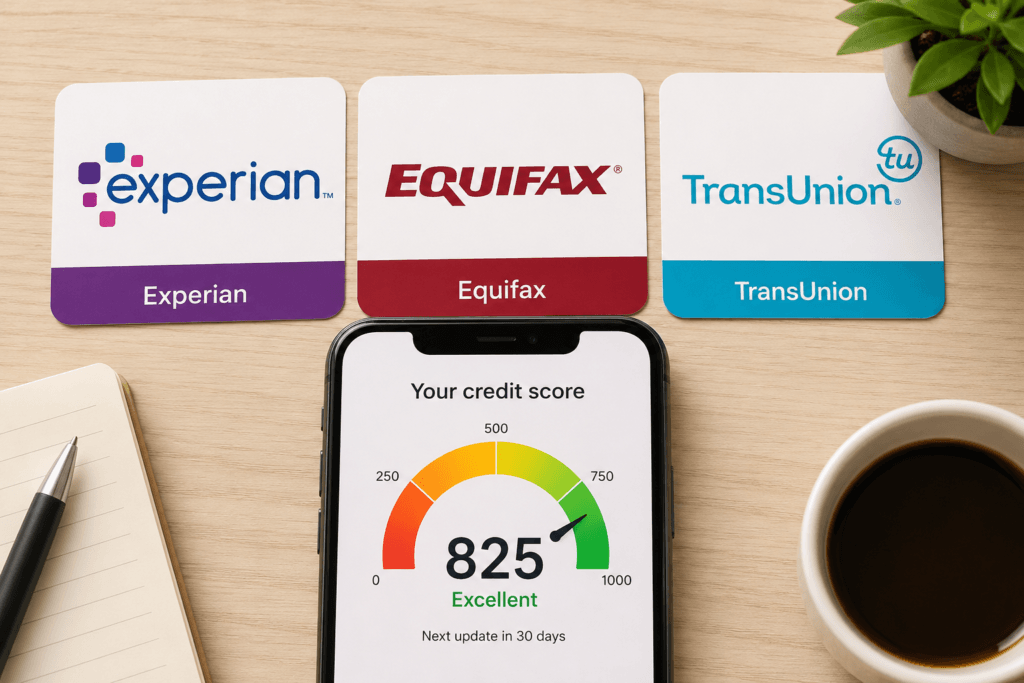

If you’ve absorbed your understanding of credit scores from American films and YouTube videos, it’s worth resetting your expectations. The UK doesn’t have a single national credit score like the US FICO system. Instead, there are three separate credit reference agencies (CRAs) — Experian, Equifax, and TransUnion — and each one holds its own data, runs its own scoring model, and uses its own scale.

This matters more than it sounds. A lender might report your mortgage to Experian but not to TransUnion. Your mobile network might report to Equifax but nowhere else. The result is that your three files can look genuinely different from one another, and the “score” you see from any single free service is really an educational estimate of how a lender might view your file — not the actual number a bank uses internally, because banks run their own scoring on top of the raw data anyway.

Experian

The largest of the three agencies in the UK and the one most commonly referenced by high-street banks and credit card providers. Experian’s own score sits on a scale running up to 999.

Equifax

Equifax holds slightly different data and is most commonly accessed through ClearScore, which presents an Equifax-based score on a scale running up to 1,000.

TransUnion

The third agency, accessed for free mainly through Credit Karma and TotallyMoney, with a scale that runs up to 710.

None of these numbers are directly comparable to each other. A “good” score on one scale can look mediocre on another purely because the maths is different — so don’t panic if your scores don’t match across services. That’s normal, not a red flag.

How to Check Your Credit Score for Free in the UK (2026) Best 3 Ways :

Here’s the practical part. These are the genuinely free options, not “free trial then charged” traps.

Experian – Free for Life

Experian offers a free version of its own credit score and report directly through its website and app, with no time limit and no card details needed at sign-up. There’s a paid CreditExpert subscription pushed fairly hard throughout the site, offering daily monitoring and extras, but it isn’t necessary if you just want to see your score and file.

ClearScore – Free Equifax Score and Report

ClearScore is arguably the most widely used free credit app in the UK, and it pulls from Equifax data. Sign-up takes a few minutes, the interface is straightforward, and the score updates monthly with email alerts when something changes.

Credit Karma and TotallyMoney – Free TransUnion Score

Both Credit Karma and TotallyMoney give free access to your TransUnion file. They work as credit brokers, meaning they earn commission when you take out a product they recommend — but viewing your score and report costs nothing regardless.

MoneySavingExpert Credit Club

MoneySavingExpert’s Credit Club is another free route to your TransUnion data, bundled with personalised eligibility checks for credit cards and loans, so you can see your approval odds before applying anywhere.

Your Statutory Credit Report — A Legal Right

Separately from all the above, you’re entitled by law to request a free statutory credit report from each CRA. This is the raw data file rather than a scored, consumer-friendly version, and Experian’s version typically arrives with a postal verification step taking a few working days. It’s worth doing once if you want the unfiltered data with none of the extras.

Comparison at a Glance

| Service | Agency Behind It | Cost | Update Frequency |

|---|---|---|---|

| Experian | Experian | Free (paid tier optional) | Continuous/on login |

| ClearScore | Equifax | Free | Monthly |

| Credit Karma | TransUnion | Free | Weekly |

| TotallyMoney | TransUnion | Free | Live/on login |

| MSE Credit Club | TransUnion | Free | Monthly |

| Statutory report | Any CRA | Free (legal right) | One-off, on request |

Realistically, most people get the fullest picture by signing up to one free service per agency — Experian for Experian, ClearScore for Equifax, and Credit Karma or TotallyMoney for TransUnion. That’s three sign-ups, about fifteen minutes total, and it covers what almost every UK lender might check.

Step-by-Step: How to Check Your Credit Score for Free in the UK (2026)?

- Pick a service — start with Experian if you’ve never checked before, since it’s the most widely referenced by lenders.

- Create an account with your name, date of birth, current address, and email.

- Verify your identity. This usually means answering a couple of questions about your financial history (an old loan, a previous address) or confirming a few digits of your bank sort code, depending on the provider.

- Wait a few minutes. Most services show your score almost immediately; a couple may take a day if extra verification is needed.

- Read your score and your full report, not just the headline number.

- Repeat with the other two agencies if you want the complete picture, especially before a mortgage or car finance application.

It really is that uncomplicated. The bit people skip — and shouldn’t — is step five.

Does Checking Your Own Credit Score Hurt It? No — Here’s Why

This is probably the most common worry, and it’s based on a genuine misunderstanding rather than nothing at all.

There are two types of credit search:

- Soft search — this happens when you check your own score, or when a company runs an eligibility check before you formally apply. It’s invisible to other lenders and has zero effect on your score.

- Hard search — this happens when you formally apply for credit. It’s visible to other lenders and can cause a small, temporary dip, particularly if you make several applications close together.

Checking your own credit score for free, through any of the services above, only ever creates a soft search. You can check it daily if you genuinely want to and nothing will change as a result of the checking itself — only as a result of what actually happens on your file, like a new account being opened or a payment being missed.

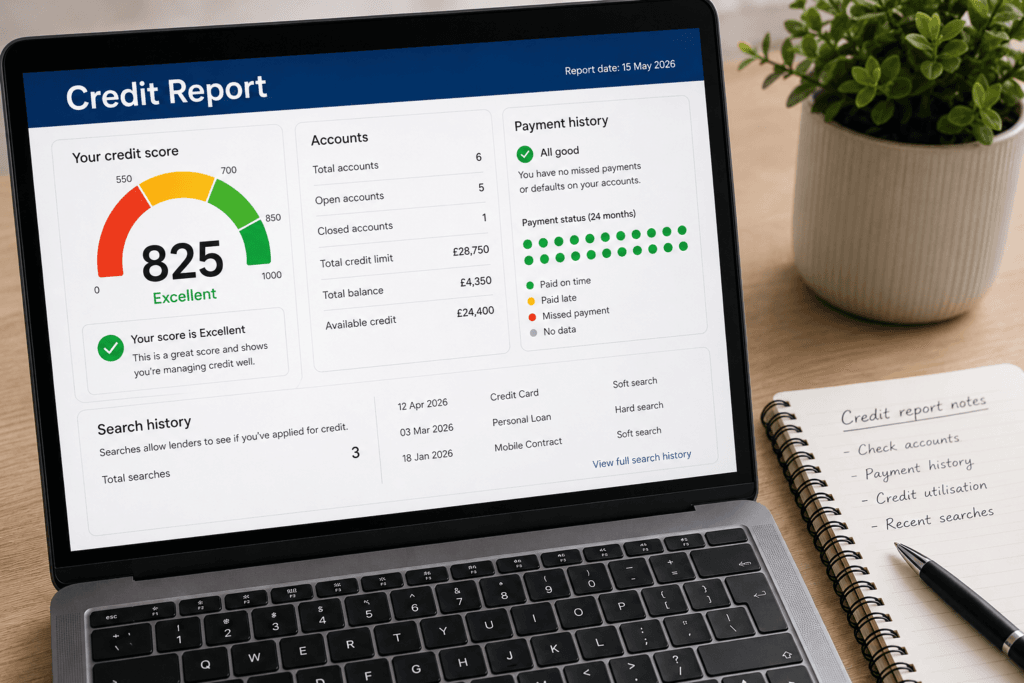

What to Actually Look At Once You’ve Got Your Report

The score is a headline. The report is where the useful information actually lives, and it’s worth going through it properly rather than glancing at the number and closing the tab.

- Accounts listed — is every one genuinely yours? Are closed accounts marked as closed?

- Payment history — are any payments flagged as late or missed that you don’t recognise?

- Financial associations — joint accounts or shared finances with an ex-partner or former housemate can drag their credit behaviour into your file. If the relationship has ended, you may need to formally disassociate.

- Defaults and County Court Judgements (CCJs) — these have a significant impact and remain on file for six years from the date they were registered, regardless of whether the debt is later settled.

- Hard searches — a long list of recent applications can be a red flag to lenders, even if each one was approved.

- Electoral roll status — being registered to vote at your current address helps lenders confirm your identity, and not being registered can quietly work against you.

How Often Should You Check Your Credit Score?

There’s no strict rule, but here’s a sensible rhythm:

- Monthly, if you like keeping an eye on things generally — it costs nothing and there’s no downside.

- At least once a year across all three agencies, since they hold different data and one might catch something the others miss.

- Three to six months before any major application — a mortgage, a car finance deal, a large personal loan — giving you time to fix anything that needs fixing before a lender sees it.

If you’re not actively planning anything, checking quarterly is more than enough to stay on top of it without becoming the kind of person who refreshes an app obsessively.

Free Ways to Improve Your Score After Checking It

Once you’ve seen where you stand, a few free, well-established steps tend to help most people:

- Register on the electoral roll at your current address via gov.uk — it’s one of the simplest identity confirmations a lender looks for.

- Use Experian Boost, a free Open Banking feature that can add positive data — council tax, subscriptions, regular bills — to your Experian file.

- Keep credit utilisation low relative to your limits, rather than maxing cards out even if you pay them off in full each month.

- Dispute genuine errors directly with the relevant CRA; they’re legally required to investigate within a set timeframe.

- Avoid clustering applications — space out credit applications rather than applying for several products in a short window.

This is a deep topic in its own right, and it’s covered properly in our guide on how to improve your credit score fast, linked below, rather than repeated here.

Common Mistakes People Make When Checking Their Credit Score for Free

- Paying when they didn’t need to. If a “free trial” asks for card details up front, it almost certainly isn’t one of the genuinely free options listed above — be cautious.

- Only checking one agency. Different lenders check different agencies, so one clean file doesn’t guarantee the others are equally tidy.

- Fixating on the number alone. A score in isolation tells you very little; the underlying report is what actually matters to a lender.

- Ignoring small errors. A wrong address or an outdated account might seem trivial, but it can complicate identity checks during a real application.

- Assuming the score they see is what the lender sees. It’s an estimate. Lenders apply their own criteria on top of the raw data.

FAQs

Is it real How to Check Your Credit Score for Free in the UK (2026)? Yes. Experian, ClearScore, Credit Karma, TotallyMoney, and MoneySavingExpert’s Credit Club all offer genuinely free access to a score and report, with no card details required and no hidden charges for the basic service.

Will checking my own credit score lower it? No. Checking your own score is recorded as a soft search, which is invisible to lenders and has no effect on your score whatsoever. Only hard searches, triggered by formal applications, can have any impact.

Which credit reference agency do lenders actually use? It varies by lender, and most don’t publicly confirm which agency or agencies they check. Many use more than one. That’s exactly why checking all three free services, rather than relying on a single one, gives you the fuller picture.

What’s the difference between a credit score and a credit report? The report is the full record of your financial history — accounts, payments, searches, addresses. The score is a simplified number generated from that data by the agency or platform showing it to you, intended as a rough, educational guide rather than the figure a lender directly uses.

Why are my Experian, ClearScore and Credit Karma scores all different? Each one draws on a different underlying agency (Experian, Equifax, and TransUnion respectively), each agency holds slightly different data because not every lender reports to all three, and each uses its own scale and formula. Differing scores across services is completely normal.

How do I get my statutory credit report instead of a scored version? You can request this directly and free of charge from Experian, Equifax, or TransUnion under UK law. It contains the raw data file without a consumer-facing score or the extra educational tools the free apps add on top.

Final Thoughts

There’s genuinely no reason to go in blind, and there’s certainly no reason to pay for something every major agency gives away free. If you take one thing from this guide, make it this: pick one free service today, create an account, and actually read through the full report rather than just glancing at the score. If you’re planning a mortgage, car finance deal, or anything similarly significant in the next year, check all three agencies and give yourself a few months’ runway to fix anything that needs fixing.

Checking your credit score for free UK-wide takes about ten minutes and tells you more about your financial standing than guessing ever will. There’s no excuse for not knowing where you stand — so go and find out.

BEST FOR YOU !

- Best Savings Accounts in the UK 2026

- How to Improve Your Credit Score Fast in the UK?: A Practical Guide for 2026

- How to Build an Emergency Fund from Scratch: 9 Smart Steps for Financial Security.

- Personal Finance for Beginners UK : A Complete Guide (2026)

Helpful External Resources

- Experian UK – free Experian credit score and statutory report requests

- ClearScore – free Equifax-based credit score and report

- Credit Karma UK – free TransUnion-based credit score and report

- MoneyHelper – free, government-backed guidance on credit and borrowing

- GOV.UK – Register to Vote – electoral roll registration

- Citizens Advice – free, independent help with credit and debt problems