TABLE OF CONTENTS

Table of Contents

Introduction

Most people in the UK are quietly losing money every year — not through bad investments or reckless spending, but simply because their savings are sitting in the wrong account.

Thank you for reading this post, don't forget to subscribe!The best savings accounts in the UK in 2026 are paying rates that haven’t been seen for well over a decade. With the Bank of England base rate having risen sharply in recent years before settling at 3.75% as of May 2026, competition among banks, building societies, and digital challengers has pushed top savings rates well above 4% — and in some categories, closer to 5% or higher.

Whether you’re building an emergency fund, saving for a house deposit, or simply trying to make your money work harder, there has rarely been a better time to review where your cash lives. This guide cuts through the noise to show you exactly what’s available, what the trade-offs are, and how to choose the right account for your circumstances.

Rates in this article are accurate to June 2026. The savings market moves quickly — always verify rates directly with providers before opening an account.

Key Takeaways

- The Bank of England base rate stands at 3.75% as of May 2026, keeping savings rates competitive relative to recent history.

- Top easy access savings accounts are paying up to 4.79% AER as of mid-June 2026.

- Regular saver accounts lead the market on headline rates, with some paying up to 7.10% AER — but with monthly deposit limits.

- The FSCS deposit protection limit increased from £85,000 to £120,000 per person, per banking licence from 1 December 2025.

- The Cash ISA annual allowance remains at £20,000 for the 2026/27 tax year — but this is the last full tax year before a new £12,000 cap takes effect from April 2027.

- Higher-rate taxpayers (earning over £50,270) should prioritise Cash ISAs, as their Personal Savings Allowance is only £500.

- NS&I Premium Bonds prize fund rate rises to 3.80% from the July 2026 draw — still trailing the top savings accounts for most holders.

- Digital challenger banks consistently offer better rates than traditional high-street banks.

Understanding the UK Savings Landscape in 2026

Before comparing individual products, it’s worth understanding the environment shaping savings rates right now.

The Bank of England made six consecutive base rate cuts between August 2024 and December 2025, taking the rate from 5.25% down to 3.75%. That trajectory has made locking in competitive fixed rates an increasingly attractive proposition for savers who want to protect returns before rates fall further.

At the same time, global uncertainty — including inflationary pressures linked to oil markets in early 2026 — has kept some rates elevated and encouraged competition among providers keen to attract deposits.

The result: savers who are prepared to shop around can still find genuinely strong returns across most account types. The biggest risk in 2026 isn’t finding a good rate — it’s settling for a mediocre one without realising it.

The Best Savings Accounts in the UK by Type

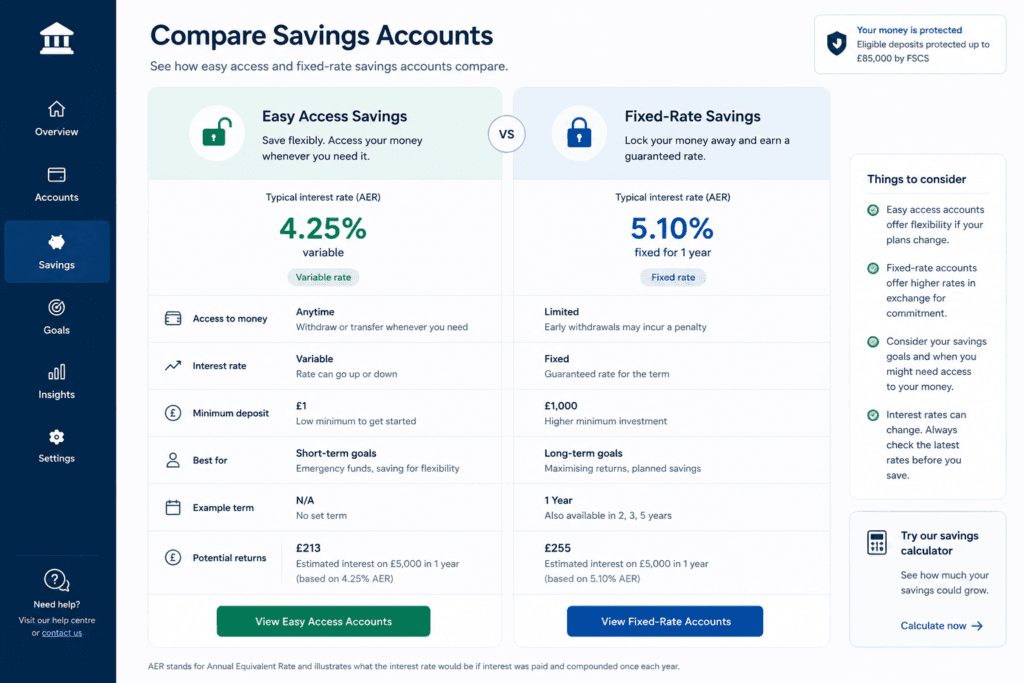

Easy Access Savings Accounts

Easy access accounts let you deposit and withdraw whenever you like, with no notice period or penalty. They’re ideal for emergency funds and money you might need at short notice.

The best easy access rates in mid-June 2026 reach up to 4.79% AER, according to money.co.uk, with several digital challengers — including Chip, Chase, and Marcus — regularly occupying top positions. High-street banks, by contrast, still pay as little as 2%–3% on some instant-access accounts, a stark reminder of how much inertia costs ordinary savers.

What to look for in an easy access account:

- Rate stability (does the rate include a short-term bonus that will drop?)

- Number of permitted withdrawals per month (some accounts limit you to 3–5 free withdrawals)

- Minimum and maximum deposit requirements

- App or online access quality

- FSCS protection status

Tip: Many easy access accounts advertise high rates that include a 12-month introductory bonus. Always check the underlying rate — the one you’ll receive after the bonus period ends. If the drop is significant, set a calendar reminder to switch before it kicks in.

Fixed-Rate Savings Bonds (Fixed-Term Accounts)

Fixed-rate bonds offer a guaranteed interest rate for a set period — typically one, two, three, or five years. In return for locking your money away, you receive a higher rate than most easy access alternatives. The catch: withdrawals during the term are usually either impossible or attract a substantial penalty.

As of June 2026, the leading one-year fixed-rate savings bond pays around 4.85% AER (MBNA Fixed Saver 1 Year, per Moneyfacts data from mid-June 2026), requiring a minimum deposit of £1,000. Five-year fixed rates are broadly similar — a relatively flat rate curve that, as one analysis notes, reflects where the market expects the base rate to sit in 2030.

When does a fixed-rate bond make sense?

A fixed bond suits you if:

- You’re confident you won’t need the money during the term.

- You believe rates will continue to fall — and want to lock in today’s returns.

- You want certainty: the same rate, every day, regardless of Bank of England decisions.

If rates rise unexpectedly during your term, you’ll miss out. Most financial planners suggest a blend: keep an accessible emergency fund (see below) and fix the portion of your savings you genuinely won’t need for 12–24 months.

Cash ISAs

A Cash ISA (Individual Savings Account) lets you save up to £20,000 per tax year — the current 2026/27 annual ISA allowance — and earn interest completely free of income tax. That allowance resets every year on 6 April and cannot be carried forward.

Important for 2026: The 2026/27 tax year (which began 6 April 2026) is the last full year savers under 65 can put up to £20,000 into a Cash ISA. From April 2027, the Cash ISA subscription limit drops to £12,000 per year. If you want to maximise your Cash ISA pot, now is the time to act.

As of May 2026, the best easy-access Cash ISA rates reach 4.76% AER from Trading 212, with Moneybox at 4.75% AER — though both include a short-term bonus element. For fixed-rate Cash ISAs, rates from RCI Bank UK, Tandem Bank, and Close Brothers reach up to 4.72% AER for one to two-year terms.

Who benefits most from a Cash ISA?

The answer depends on your tax position:

| Tax Band | Annual Income | Personal Savings Allowance | ISA Benefit |

|---|---|---|---|

| Basic rate | £12,571 – £50,270 | £1,000 | Moderate – useful if savings are large |

| Higher rate | £50,271 – £125,140 | £500 | High – tax-free interest is valuable |

| Additional rate | Over £125,140 | £0 | Essential – no PSA outside an ISA |

| Non-taxpayer | Under £12,570 | £1,000 | Low – PSA likely covers most interest |

For higher-rate taxpayers with significant savings, a Cash ISA is almost always the right starting point. For basic-rate taxpayers with more modest pots, the Personal Savings Allowance may cover all interest earned — but once you approach the threshold, an ISA pays dividends.

Important: If you transfer a Cash ISA to a new provider, always use the formal ISA transfer process. If you withdraw the money yourself and redeposit it elsewhere, you’ll use up new ISA allowance unnecessarily. Contact the receiving provider and ask them to handle the transfer paperwork.

Regular Savings Accounts

Regular saver accounts require you to deposit a fixed amount every month — typically between £25 and £500 — and in return, offer the highest headline rates on the market. As of June 2026, the top rates include:

- Zopa – 7.10% variable (for existing customers, for six months)

- First Direct – 7.00% fixed

- Co-op Bank – 7.00% variable

- Monmouthshire Building Society – 6.00% variable (open to all)

These rates sound exceptional — and for the right saver, they are. But there are important limitations:

- Monthly deposit caps (usually £200–£500) mean the total interest earned in pounds is modest.

- Rates are often available only to existing current account holders.

- Some accounts only pay interest at the end of 12 months.

- Missing a monthly deposit can result in the rate dropping.

Example: If the maximum monthly deposit is £300 at 7.00%, your average balance over 12 months is roughly £1,950. The interest earned would be approximately £136 — useful, but not life-changing. The real value of regular savers is the discipline they build around saving consistently, combined with a genuinely strong rate on the amount deposited.

(For more on making saving a habit, see our guide to budgeting basics for UK households.)

Notice Savings Accounts

Notice accounts sit between easy access and fixed-rate bonds. You can withdraw your money — but must give a specified notice period first, typically 30, 60, 90, or 120 days. In return, you earn a higher rate than most easy access accounts, without the full commitment of a fixed-rate bond.

As of mid-June 2026, RCI Bank UK’s 14-day notice account pays 4.00% AER — a competitive rate for a relatively short notice period, with a minimum opening deposit of £100.

Notice accounts work well for money you’re confident you won’t need urgently but may want to access within the next few months — a planned purchase, an upcoming tax bill, or a house-related cost.

NS&I Premium Bonds

Premium Bonds are the UK’s most popular savings product, with over 22 million holders. Issued by NS&I (National Savings & Investments) and backed 100% by HM Treasury, they offer total capital protection well beyond the FSCS limit — a genuine advantage for savers with larger pots.

Instead of interest, you enter a monthly prize draw. Prizes range from £25 to £1 million and are completely tax-free regardless of your income. The prize fund rate is rising to 3.80% AER from the July 2026 draw — the first increase in almost three years, following a series of cuts that took the rate from 4.65% in late 2023.

However, 3.80% is a statistical average across all bondholders. Most people with average luck earn considerably less than the headline rate. For savers who have already filled their Cash ISA and exhausted their Personal Savings Allowance, the tax-free prize element adds genuine value. For everyone else, the best standard savings accounts and ISAs comfortably beat Premium Bonds on expected return.

Maximum holding: £50,000 per person.

Lifetime ISA (LISA)

The Lifetime ISA deserves a mention for those saving specifically for a first home or retirement. You can contribute up to £4,000 per tax year, and the government adds a 25% bonus — up to £1,000 per year — on top.

The important catch: withdrawing for any reason other than buying your first home (worth up to £450,000) or reaching age 60 triggers a 25% withdrawal penalty — which effectively takes back the bonus and more. Use a LISA only if you’re certain about your goal and timeline.

(Thinking about your first home purchase? See our guide to Help to Buy alternatives and first-time buyer schemes in the UK.)

Tax on Savings Interest: What Every UK Saver Needs to Know

With savings rates now meaningfully above zero, tax on savings interest has become relevant for many more people than it was two or three years ago.

The Personal Savings Allowance (PSA)

The Personal Savings Allowance lets you earn a set amount of interest tax-free each year, outside of an ISA:

| Tax Band | Annual Income | Personal Savings Allowance |

|---|---|---|

| Basic rate | Up to £50,270 | £1,000 |

| Higher rate | £50,271 – £125,140 | £500 |

| Additional rate | Over £125,140 | £0 |

At current top rates (around 4.5%–5%), a basic-rate taxpayer with roughly £22,000 or more in non-ISA savings will start paying tax on their interest. For higher-rate taxpayers, the threshold is closer to £11,000. Above these amounts, every pound of interest beyond the allowance is taxed at your marginal income tax rate (20%, 40%, or 45%).

Banks report interest directly to HMRC — you don’t need to declare it manually unless you file a Self Assessment return. HMRC typically adjusts your tax code the following year to collect any tax owed.

The Starting Rate for Savings

If your non-savings income is below £17,570, you may be eligible for the Starting Rate for Savings — an additional £5,000 of tax-free savings interest on top of the PSA. This is particularly valuable for retirees and lower-income earners with larger savings pots.

(For more on managing your tax position as a saver, see our guide to ISAs explained: every type compared.)

FSCS Protection: How Safe Is Your Money?

The Financial Services Compensation Scheme (FSCS) protects deposits held with authorised UK banks and building societies. From 1 December 2025, the protection limit increased from £85,000 to £120,000 per person, per banking licence (£240,000 for joint accounts).

This is significant for savers with larger pots. One important catch: several well-known bank brands share a single banking licence. HSBC and First Direct, for example, are covered by the same licence — meaning deposits across both are protected to a combined total of £120,000, not £120,000 each.

If you have savings above £120,000, spread them across providers operating under genuinely separate licences. The FSCS website has a checker tool to verify which banks share licences.

For amounts above FSCS limits, NS&I is the only provider offering unlimited, 100% Treasury-backed protection — though at rates that typically trail the top challenger banks by 0.5% or more.

Practical Examples: Choosing the Right Account

Scenario 1: The Emergency Fund Builder

Profile: Amir has just started taking saving seriously. He wants to keep three to six months of expenses accessible at all times.

Best choice: An easy access savings account paying a competitive variable rate (aim for at least 4%+ AER). Keep it separate from his current account to avoid temptation. If this is his only pot and the interest earned is under £1,000, tax won’t be an issue initially.

(For guidance on how much to hold in an emergency fund, see our dedicated guide to emergency funds in the UK.)

Scenario 2: The Higher-Rate Taxpayer With £50,000 to Save

Profile: Gemma earns £65,000 and has £50,000 to save. Her Personal Savings Allowance is only £500. At 4.5% AER, she’d earn around £2,250 in interest — meaning £1,750 is taxable at 40%, costing her £700 in tax.

Best choice:

- Use her full £20,000 ISA allowance in a competitive Cash ISA (up to 4.76% AER tax-free).

- Invest the remaining £30,000 in a fixed-rate bond — accepting some tax on that portion, but maximising the tax-free element first.

This approach shelters £20,000 of interest-generating capital from tax entirely, reducing her tax bill significantly.

Scenario 3: The Cautious Saver With £180,000

Profile: Derek is retired, cautious, and has £180,000 in cash savings.

Best choice:

- £20,000 into a Cash ISA (tax-free, FSCS protected).

- £100,000 split across two or three separate banking licences in easy access or fixed-rate accounts (staying under £120,000 per licence).

- £50,000 into NS&I Premium Bonds — fully government-backed above the FSCS limit, with tax-free prizes as a bonus.

This strategy protects all of Derek’s capital, maximises tax efficiency, and spreads risk sensibly.

Common Savings Mistakes to Avoid in 2026

Leaving Money in a Default Current Account

Many UK current accounts pay 0% to 1.5% on balances. With easy access savings accounts paying over 4%, leaving a significant balance in a current account is one of the most common and costly financial habits in the UK.

Ignoring the Post-Bonus Rate

Promotional rates can look dazzling. An account advertising 5.5% AER might revert to 2% after 12 months. Always note the revert rate and set a diary reminder to review and switch when it drops.

Not Splitting Savings Above £120,000

The FSCS limit is per banking licence — not per account. If you have over £120,000 with one provider (or provider group), the excess is unprotected. This is no longer a niche concern: with savings rates where they are, this issue affects more people than many expect.

Treating All Fixed-Rate Bonds as Accessible

Fixed-rate bonds are genuinely illiquid for most practical purposes. Locking money you’ll actually need for a house purchase, tax bill, or major expense into a two-year fixed bond creates real problems. Only fix money you’re genuinely certain you won’t need during the term.

Forgetting the Cash ISA Allowance Deadline

The ISA allowance resets on 6 April and cannot be carried forward. Every year it goes unused is a year of tax-free capacity lost permanently. With the Cash ISA cap set to reduce to £12,000 from April 2027, the current 2026/27 tax year is the last chance to shelter up to £20,000 in a Cash ISA.

Choosing a Provider Based on Name Recognition Alone

High-street familiarity is not a proxy for better rates. Digital challengers such as Chip, Atom Bank, Tandem, Zopa, and Trading 212 all carry full FSCS protection and consistently offer more competitive rates than the traditional big banks. The rate difference, not the brand, is what matters for your returns.

Comparison Table: Best Savings Account Types in the UK (June 2026)

| Account Type | Best Rate (Approx.) | Access | Best For | Key Risk |

|---|---|---|---|---|

| Easy Access | Up to 4.79% AER | Instant | Emergency funds, short-term savings | Rate can change at any time |

| Fixed-Rate Bond (1 year) | Up to 4.85% AER | Locked in | Medium-term savings | No access without penalty |

| Cash ISA (Easy Access) | Up to 4.76% AER | Instant | Tax-efficient saving | Bonus rates may drop |

| Cash ISA (Fixed) | Up to 4.72% AER | Locked in | Higher-rate taxpayers | Rate locked, no access |

| Regular Saver | Up to 7.10% AER | Annual (typical) | Building a savings habit | Low deposit caps |

| Notice Account (30-day) | Up to 4.00% AER | 14–30 days’ notice | Planned near-future expenses | Must wait to access funds |

| NS&I Premium Bonds | 3.80% prize fund rate | Instant | Capital protection, tax-free prizes | Not a guaranteed return |

Rates correct to June 2026. Verify with providers before applying.

Frequently Asked Questions

What is the best savings account in the UK right now?

It depends entirely on your circumstances. If you want instant access, top easy access accounts pay up to 4.79% AER. For guaranteed returns over one to two years, fixed-rate bonds offer up to 4.85% AER. For tax-efficiency, a Cash ISA is usually the smartest starting point. There is no single best account — the right answer depends on your tax position, timeline, and need for flexibility.

Are savings rates likely to fall in 2026?

The Bank of England held the base rate at 3.75% for two consecutive meetings as of mid-2026. Market forecasts suggest gradual further cuts are possible, though global uncertainty has made predictions less reliable. If rates fall, variable easy access rates will drop. Fixed-rate bonds allow you to lock in current rates before any cuts take effect.

How much of my savings are protected by the FSCS?

Since 1 December 2025, the FSCS protects up to £120,000 per person, per banking licence (£240,000 for joint accounts). This applies to all UK-authorised banks and building societies. Be aware that some familiar bank brands share a licence — check the FSCS checker tool before spreading savings across brands you assume are separate.

Should I use a Cash ISA or a standard savings account?

For higher-rate or additional-rate taxpayers, a Cash ISA is almost always preferable, as it shelters all interest from tax regardless of the amount. For basic-rate taxpayers, the £1,000 Personal Savings Allowance means a standard savings account is sufficient unless you have significant savings (roughly £22,000+ at current rates). Once you approach that threshold, switching to an ISA makes sense.

Can I have multiple savings accounts at the same time?

Yes. There is no limit on how many savings accounts you can hold. Many savers benefit from keeping multiple accounts: an easy access account for emergencies, a fixed-rate bond for medium-term savings, and a Cash ISA for tax efficiency. You can only open one Lifetime ISA, however.

Are challenger bank savings accounts safe?

Yes — as long as they are authorised by the Financial Conduct Authority (FCA) and covered by the FSCS. Digital banks such as Chip, Atom, Tandem, Zopa, and Trading 212 all carry FSCS protection to the same £120,000 limit as high-street banks. Their higher rates reflect lower overheads (no branches), not higher risk.

Is it worth having a Lifetime ISA (LISA)?

Only if you’re saving specifically for a first home purchase (on a property worth up to £450,000) or for retirement after age 60. The 25% government bonus is genuinely valuable, but the 25% withdrawal penalty for any other use makes a LISA unsuitable for general savings. If you meet the criteria, it’s one of the best government-backed incentives available for UK savers.

What happens to my savings if a bank goes bust?

If the bank is FSCS-registered, your savings up to £120,000 per banking licence are protected and would be returned to you — typically within seven working days under current FSCS rules. Above that amount, you are an unsecured creditor of the bank, meaning recovery is uncertain and potentially partial. This is why spreading large sums across separate banking groups matters.

Conclusion

The best savings accounts in the UK in 2026 offer genuinely strong returns for savers who take the time to compare and choose carefully. With top easy access rates above 4.75%, fixed-rate bonds approaching 5%, and regular savers paying over 7%, the reward for switching away from a lazy default account can be hundreds — even thousands — of pounds extra per year.

The three most important decisions for UK savers in 2026 are:

- Tax wrapper first: Use your Cash ISA allowance before it falls to £12,000 from April 2027. This is especially urgent for higher-rate taxpayers.

- Fixed or flexible: Decide how much of your savings you genuinely won’t need for one to two years, and consider fixing that portion to lock in rates before potential cuts.

- FSCS awareness: If you’re saving above £120,000, spread across genuinely separate banking licences — or use NS&I for unlimited Treasury-backed security on amounts above the FSCS threshold.

The difference between the best savings rate and the average high-street rate on a £30,000 pot is easily £600 per year or more. That’s not a rounding error — it’s a meaningful sum that compounds over time.

Start with where your money is today. Then ask whether it’s really working as hard as it could be.

Final Actionable Tips

- Today: Check your current savings account rate. If it’s below 3.5%, you’re almost certainly leaving money on the table.

- This week: Open a free account with one of the major comparison tools (Moneyfacts, MoneySuperMarket, or MoneySavingExpert’s savings section) and compare your current rate against the market.

- This month: Use your Cash ISA allowance for this tax year — especially if you’re a higher-rate taxpayer. This is the last full year before the annual Cash ISA cap reduces to £12,000.

- If you have over £10,000: Consider splitting between an easy access account (emergency fund portion) and a one-year fixed-rate bond (remainder you won’t need soon).

- Set a reminder: Variable savings rates change regularly. Review your savings accounts every six months and switch if the rate has dropped significantly below the market leader.

Opportunities

The following related articles would make natural internal links within this content:

- “How to Build an Emergency Fund in the UK” — link from the easy access / Amir scenario sections.

- “Budgeting Basics: How to Take Control of Your Monthly Finances” — link from the regular savings account section.

- “How to Improve Your Credit Score Fast in the UK” — link from the introduction as part of a financial health framework.

- “ISAs Explained: Every Type Compared” — link from the Cash ISA and tax sections.

- “How to Invest in the UK: A Starter Guide for Beginners” — link from the conclusion as a next step once savings are optimised.

- “Help to Buy Alternatives: First-Time Buyer Schemes Explained” — link from the Lifetime ISA section.

References :

- MoneyHelper — Cash ISAs Explained https://www.moneyhelper.org.uk/en/savings/types-of-savings/cash-isas

- MoneyHelper — Tax on Savings and Investments https://www.moneyhelper.org.uk/en/savings/types-of-savings/tax-on-savings-and-investments

- NS&I Corporate — Improved Rates for Premium Bonds and NS&I Savings Accounts (May 2026) https://nsandi-corporate.com/news-research/news/improved-rates-premium-bonds-and-four-other-nsi-savings-accounts

- Financial Services Compensation Scheme (FSCS) — FSCS Protection Limit Increase to £120,000 https://www.fscs.org.uk

- GOV.UK — ISA Allowances and Rules https://www.gov.uk/individual-savings-accounts