TABLE OF CONTENTS

Table of Contents

Life has a habit of throwing financial surprises at us when we least expect them. A sudden boiler breakdown, an unexpected car repair, redundancy, or even a medical-related expense can quickly put pressure on your finances. That’s why one of the most important questions in personal finance is: How Much Emergency Fund Do You Need?

Thank you for reading this post, don't forget to subscribe!Many people know they should have an emergency fund, but far fewer know how much they actually need to save. Some financial experts suggest three months of expenses, while others recommend six months or even more. The truth is that the right amount depends on your personal circumstances, income stability, family situation, and financial commitments.

In this guide, you’ll learn exactly how to calculate your ideal emergency fund, avoid common mistakes, decide where to keep your savings, and build a financial safety net that gives you genuine peace of mind.

What Is an Emergency Fund?

An emergency fund is money set aside specifically for unexpected expenses or financial emergencies.

Unlike savings for holidays, home improvements, or Christmas spending, an emergency fund exists to protect you from genuine financial shocks.

Typical emergencies include:

- Losing your job

- Sudden illness preventing work

- Emergency home repairs

- Car breakdowns

- Unexpected travel due to family emergencies

- Essential appliance replacement

An emergency fund acts as a financial buffer, helping you avoid relying on credit cards, overdrafts, or loans when life doesn’t go according to plan.

Think of it as financial insurance that you create for yourself.

Why Having an Emergency Fund Matters More Than Ever

The UK economy has experienced significant uncertainty over recent years. Rising living costs, higher mortgage rates, energy price fluctuations, and changing employment conditions have highlighted the importance of financial resilience.

Without emergency savings, even relatively small unexpected expenses can create long-term financial problems.

For example:

Imagine your washing machine breaks down and replacement costs £450.

If you have an emergency fund:

- You pay the bill.

- Life continues normally.

If you don’t:

- You put the expense on a credit card.

- Interest accumulates.

- Your debt increases.

- Future finances become more stressful.

The difference may seem small initially, but repeated unexpected expenses can significantly impact your financial health.

How Much Emergency Fund Do You Need?

This is the question most people ask.

The traditional advice is:

| Situation | Recommended Emergency Fund |

|---|---|

| Stable employment | 3 months of expenses |

| Variable income | 6 months of expenses |

| Self-employed | 6–12 months of expenses |

| Single income household | 6 months+ |

| Multiple dependants | 6–12 months |

However, these figures should be viewed as guidelines rather than strict rules.

Your ideal emergency fund depends on your own circumstances.

Let’s break it down properly.

Calculate Your Essential Monthly Expenses

Before deciding how much emergency fund you need, calculate your essential monthly spending.

Focus only on necessities.

Include:

- Rent or mortgage

- Council tax

- Utilities

- Food and groceries

- Insurance

- Transportation

- Mobile phone

- Broadband

- Childcare

- Debt repayments

Avoid including:

- Holidays

- Entertainment subscriptions

- Dining out

- Shopping

- Luxury spending

For example:

| Essential Expense | Monthly Cost |

|---|---|

| Mortgage | £1,000 |

| Council Tax | £180 |

| Utilities | £250 |

| Food | £400 |

| Transport | £200 |

| Insurance | £120 |

| Other essentials | £150 |

| Total | £2,300 |

If your essential monthly expenses are £2,300, then:

- 3-month fund = £6,900

- 6-month fund = £13,800

- 12-month fund = £27,600

This provides a realistic target based on your actual lifestyle.

Factors That Affect Your Emergency Fund Size

Job Security

Someone working in a highly stable sector may need a smaller emergency fund than someone in a volatile industry.

Ask yourself:

- How easily could I find another job?

- Is my industry currently growing or shrinking?

- Does my employer appear financially stable?

The less certainty you have, the larger your emergency fund should be.

Self-Employment and Freelance Income

Self-employed individuals face greater income variability.

One month may be excellent, while the next may be quieter than expected.

Because of this uncertainty, many financial planners suggest saving between six and twelve months of essential expenses.

Freelancers, contractors, consultants, and business owners should generally aim for a larger financial cushion.

Family Responsibilities

If other people depend on your income, the stakes are higher.

This includes:

- Children

- Partners

- Elderly relatives

A larger emergency fund provides additional protection for your household.

Health Considerations

Although the NHS provides extensive healthcare support, illness can still affect your finances.

You may experience:

- Reduced working hours

- Travel expenses

- Care costs

- Temporary income disruption

Those with health concerns may benefit from holding extra emergency savings.

The Difference Between a Starter Fund and a Full Emergency Fund

Building a large emergency fund can feel overwhelming.

The good news?

You don’t need to save everything immediately.

Many people start with a “mini emergency fund.”

Starter Emergency Fund

Aim for:

£500–£1,000

This can cover:

- Minor car repairs

- Appliance breakdowns

- Unexpected bills

It’s a realistic first milestone and provides immediate protection.

Full Emergency Fund

Once your starter fund is complete, work towards:

- Three months of expenses

- Then six months

- Then more if appropriate

Breaking the process into stages makes the goal feel achievable.

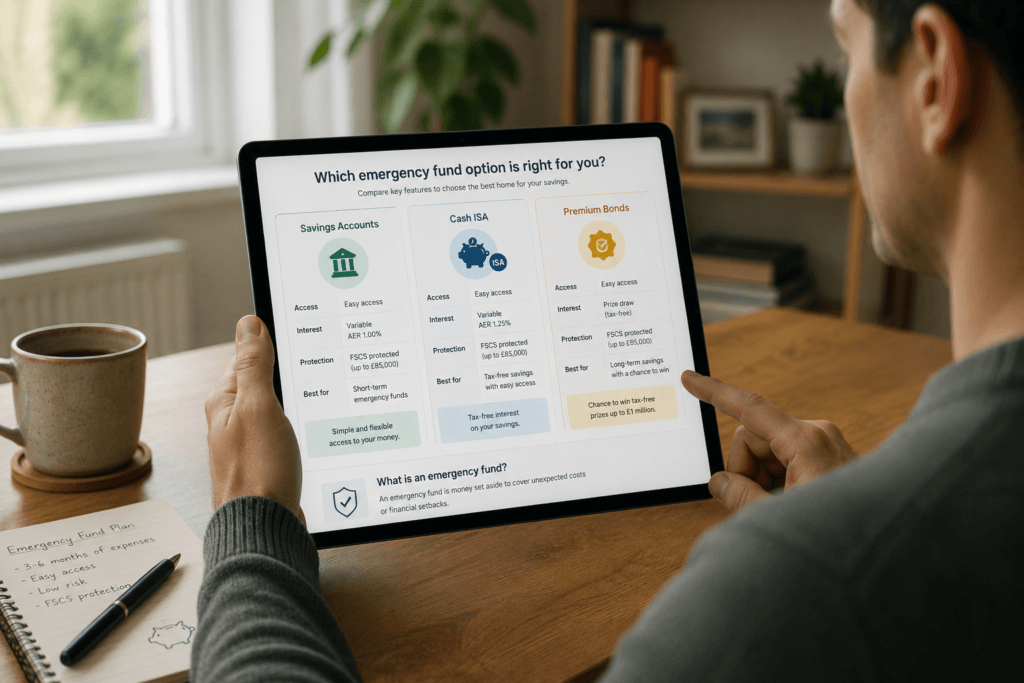

Where Should You Keep Your Emergency Fund?

The primary purpose of an emergency fund is accessibility.

You need quick access when emergencies happen.

That means avoiding investments that may fluctuate in value.

Good options include:

Easy-Access Savings Accounts

Advantages:

- Quick access

- Interest earnings

- Low risk

Many UK savers choose easy-access savings accounts for emergency funds.

Cash ISAs

Cash ISAs can provide tax-efficient savings while maintaining accessibility.

However, ensure withdrawal restrictions don’t interfere with emergency access.

Premium Bonds

Some people keep part of their emergency fund in Premium Bonds.

Benefits include:

- Capital security

- Prize draw opportunities

- Government-backed savings

However, access is not always as immediate as a standard savings account.

Avoid Investing Emergency Savings

Emergency funds should generally not be invested in:

- Individual shares

- ETFs

- Cryptocurrency

- High-risk investments

Markets can decline precisely when you need access to your money.

Your emergency fund’s job is protection, not growth.

Common Emergency Fund Mistakes

Saving Too Little

Many people underestimate how much financial disruption can cost.

One unexpected event can easily exceed £1,000.

Building adequate reserves matters.

Saving Too Much in Cash

This might sound surprising.

Once your emergency fund target is reached, keeping excessive amounts in low-interest cash accounts may slow long-term wealth building.

Beyond your emergency fund, surplus savings may be better allocated towards:

- Investing

- Pension contributions

- Mortgage overpayments

Depending on your goals.

Using the Fund for Non-Emergencies

A discounted holiday is not an emergency.

Neither is a new television.

Create separate savings pots for planned purchases.

Protect your emergency fund for genuine emergencies only.

Not Replacing Withdrawn Funds

If you use part of your emergency fund, rebuild it as soon as practical.

Your safety net only works when it’s fully funded.

How to Build an Emergency Fund Faster

Building savings can seem difficult, especially with rising living costs.

However, small consistent actions often produce impressive results.

Automate Savings

Set up an automatic transfer immediately after payday.

Even £50–£100 per month can build significant savings over time.

Save Windfalls

Consider directing:

- Bonuses

- Tax refunds

- Cashback rewards

- Gift money

Into your emergency fund.

These occasional boosts can accelerate progress dramatically.

Review Subscriptions

Many households spend hundreds of pounds annually on subscriptions they rarely use.

Cancelling unused services can free up money for savings.

Use Budgeting Apps

Budgeting apps can help identify spending leaks and create additional saving opportunities.

Even small adjustments can compound over time.

Increase Income Temporarily

Some people build emergency funds faster through:

- Freelance work

- Overtime

- Selling unused items

- Side projects

A short-term effort can create long-term financial security.

Should You Build an Emergency Fund Before Investing?

This is one of the most common personal finance questions.

Generally speaking, yes.

Before investing heavily in shares or funds, having some emergency savings in place is wise.

Why?

Without emergency savings, you may be forced to sell investments during a market downturn to cover unexpected expenses.

That can lock in losses and disrupt your long-term strategy.

A balanced approach often works best:

- Build a starter emergency fund.

- Pay off expensive debt.

- Grow emergency savings.

- Begin investing regularly.

This creates a stronger financial foundation.

Emergency Funds and Credit Scores

Although emergency funds do not directly affect your credit score, they can indirectly improve your financial profile.

When unexpected expenses arise, emergency savings help you avoid:

- Missed payments

- Overdraft reliance

- Credit card debt accumulation

- Loan applications during emergencies

Maintaining healthy finances often contributes to better long-term credit behaviour.

Emergency Funds for Homeowners vs Renters

Homeowners

Homeowners often need larger emergency funds because unexpected repairs can be costly.

Examples:

- Boiler replacement

- Roof repairs

- Plumbing issues

- Electrical work

A homeowner’s emergency fund should reflect these potential expenses.

Renters

Renters may have fewer property maintenance responsibilities but still need protection against:

- Job loss

- Rent increases

- Relocation costs

- Household emergencies

Emergency savings remain essential regardless of housing status.

How Much Emergency Fund Do You Need If You Have Debt?

The answer depends on the type of debt.

High-Interest Debt

If you’re carrying expensive credit card debt, balancing repayment and emergency savings is usually sensible.

Many financial experts suggest:

- Build a small emergency fund first

- Then aggressively tackle high-interest debt

- Continue expanding savings afterwards

Low-Interest Debt

For lower-interest borrowing such as some mortgages or student finance arrangements, maintaining a larger emergency fund may be appropriate.

Every financial situation is different, so consider your own risk tolerance and cash flow needs.

A Real-Life Emergency Fund Example

Let’s imagine Sarah lives in Manchester.

Her essential monthly expenses total £2,100.

She works in marketing and feels reasonably secure in her role.

Her target:

- Starter fund: £1,000

- Three-month fund: £6,300

- Long-term target: £12,600

She saves:

- £250 monthly

- Annual bonus contributions

- Cashback rewards

Within two years, she reaches her six-month target.

When her boiler unexpectedly fails during winter, she pays for repairs without debt or financial panic.

That’s exactly what an emergency fund is designed to do.

BEST FOR YOU !

- Personal Finance for Beginners UK : A Complete Guide (2026)

- How to Build an Emergency Fund from Scratch: 9 Smart Steps for Financial Security.

- Best Cashback Credit Cards for Everyday Spending in the UK

- Why Your Credit Score Dropped and How to Fix It?

- Stocks vs ETFs: Which Investment Is Better? 2026-2027

- How Credit Score Mistakes That Could Cost You Thousands in the UK? 2026

- Best Cashback Credit Cards in the UK for 2026-2027

- What is a Good Credit Score in the UK?

Helpful External Resources

- MoneyHelper – https://www.moneyhelper.org.uk

- FCA (Financial Conduct Authority) – https://www.fca.org.uk

- Citizens Advice – https://www.citizensadvice.org.uk

- Bank of England – https://www.bankofengland.co.uk

- GOV.UK – https://www.gov.uk

FAQs

How much emergency fund do I need in the UK?

Most UK households should aim for three to six months of essential living expenses. Those with irregular income or dependants may benefit from six to twelve months of expenses.

Is £1,000 enough for an emergency fund?

£1,000 is an excellent starting point and can cover many common emergencies. However, most people should eventually build a larger fund based on their monthly expenses.

Where should I keep my emergency fund?

Easy-access savings accounts are generally the most practical option because they offer quick access while keeping your money safe.

Should I invest my emergency fund?

Emergency funds are typically better kept in cash-based savings products rather than investments because you may need immediate access during market downturns.

Can I build an emergency fund while paying off debt?

Yes. Many people start with a small emergency fund before focusing on high-interest debt repayment and then continue expanding their savings afterwards.

How long does it take to build an emergency fund?

The timeline depends on your income and savings rate. Saving consistently every month, even in small amounts, can build a meaningful emergency fund over time.

Final Thoughts

If you’ve been wondering How Much Emergency Fund Do You Need?, the answer ultimately comes down to your personal circumstances. While three to six months of essential expenses is a useful guideline, your employment stability, family responsibilities, debt levels, and financial goals all play a role.

The most important step isn’t achieving a perfect target overnight. It’s getting started. Even a modest emergency fund can provide valuable protection against life’s unexpected costs.

Begin by calculating your essential monthly expenses, set a realistic savings target, automate contributions where possible, and build your safety net gradually. Future-you will almost certainly be grateful you did.