TABLE OF CONTENTS

Table of Contents

Introduction

If you have ever applied for a credit card, personal loan, mortgage, or mobile phone contract, you have probably heard about credit scores. Many people ask, “What is a Good Credit Score in the UK” because lenders often use credit information to assess whether an applicant is financially responsible.

Thank you for reading this post, don't forget to subscribe!Understanding your credit score is one of the most important steps toward managing your personal finances effectively. A strong credit score can improve your chances of being approved for financial products and may even help you access more competitive interest rates.

In this comprehensive guide, we will explain What is a Good Credit Score in the UK, how credit scores work, what factors affect them, and how you can improve your score over time.

What Is a Credit Score?

A credit score is a numerical representation of your creditworthiness. It helps lenders determine how likely you are to repay borrowed money on time.

In the UK, there is no single universal credit score. Instead, different credit reference agencies use their own scoring systems.

The three main credit reference agencies are:

Each agency collects financial information and calculates your score differently.

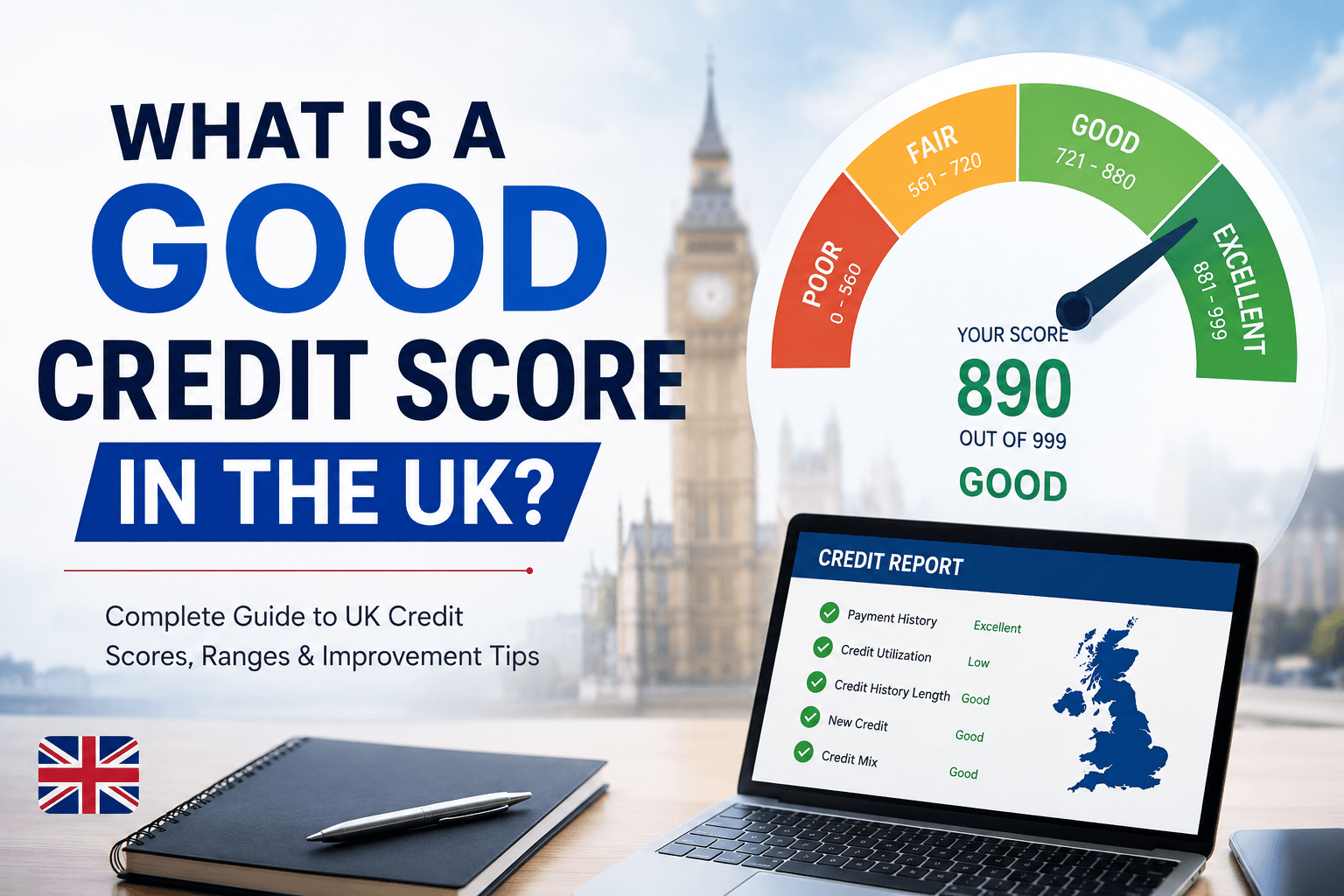

What Is a Good Credit Score in the UK?

The answer depends on which credit reference agency you are using.

Experian Credit Score Ranges

| Score | Rating |

|---|---|

| 0 – 560 | Very Poor |

| 561 – 720 | Poor |

| 721 – 880 | Fair |

| 881 – 960 | Good |

| 961 – 999 | Excellent |

A score between 881 and 960 is generally considered a good credit score according to Experian.

Equifax Credit Score Ranges

| Score | Rating |

|---|---|

| 0 – 438 | Poor |

| 439 – 530 | Fair |

| 531 – 670 | Good |

| 671 – 810 | Very Good |

| 811 – 1000 | Excellent |

A score between 531 and 670 is considered good.

TransUnion Credit Score Ranges

| Score | Rating |

|---|---|

| 0 – 550 | Very Poor |

| 551 – 565 | Poor |

| 566 – 603 | Fair |

| 604 – 627 | Good |

| 628 – 710 | Excellent |

A score above 604 is generally considered good.

Why Is a Good Credit Score Important?

A good credit score can provide several financial advantages.

Easier Loan Approval

Lenders are more likely to approve applications from borrowers with strong credit histories.

Better Interest Rates

A higher score may help you qualify for lower interest rates.

Higher Credit Limits

Credit card providers may offer larger credit limits to individuals with good credit.

Better Mortgage Opportunities

Mortgage lenders often review your credit profile before approving applications.

Improved Financial Reputation

Your credit score reflects your financial responsibility and borrowing behavior.

How Is Your Credit Score Calculated?

Many people wonder how credit reference agencies determine their scores.

Several factors contribute to your overall rating.

1. Payment History

This is one of the most important factors.

Paying bills and credit commitments on time demonstrates financial reliability.

Late payments can negatively impact your score.

2. Credit Utilization

Credit utilization refers to how much of your available credit you are using.

For example:

- Credit Limit: £5,000

- Balance: £1,000

Utilization = 20%

Financial experts generally recommend keeping utilization below 30%.

3. Length of Credit History

Older accounts often help demonstrate long-term responsible borrowing behavior.

4. Credit Applications

Submitting multiple credit applications within a short period may negatively affect your score.

5. Public Records

County Court Judgments (CCJs), bankruptcies, and Individual Voluntary Arrangements (IVAs) can significantly reduce your score.

6. Electoral Roll Registration

Being registered on the electoral roll helps lenders verify your identity.

Image: Understanding Credit Scores

What Is Considered a Bad Credit Score?

A bad credit score generally falls within the poor or very poor categories.

Common reasons include:

- Missed payments

- High debt levels

- Defaults

- CCJs

- Bankruptcy

- Frequent credit applications

A low score does not permanently prevent you from accessing credit, but it may limit your options.

How to Check Your Credit Score in the UK

Checking your score regularly is an important part of financial management.

You can obtain your credit report from:

Experian

Official Website:

https://www.experian.co.uk

Equifax

Official Website:

https://www.equifax.co.uk

TransUnion

Official Website:

https://www.transunion.co.uk

Regular monitoring helps identify errors and track improvements.

Does Checking Your Credit Score Lower It?

No.

Checking your own credit score is considered a soft search and does not negatively affect your rating.

Only hard credit checks performed during loan or credit card applications may impact your score.

What Credit Score Do You Need for a Mortgage?

There is no specific mortgage score requirement.

Each lender has its own criteria.

However, having a good or excellent credit score generally improves your chances of approval and may help you secure better mortgage deals.

Mortgage providers also consider:

- Income

- Employment status

- Existing debts

- Deposit amount

- Affordability

How to Improve Your Credit Score in the UK

If you are asking “What is a Good Credit Score in the UK”, you may also be interested in improving your score.

Here are proven strategies.

Pay Bills on Time

Consistent payments help build a strong credit profile.

Consider setting up direct debits for recurring bills.

Register on the Electoral Roll

This simple step can strengthen your credit profile.

Reduce Credit Card Balances

Lower balances can improve your credit utilization ratio.

Avoid Multiple Applications

Applying for several financial products at once can create risk signals for lenders.

Keep Old Accounts Open

Long-standing credit accounts can contribute positively to your credit history.

Check Your Credit Report

Review your report regularly for inaccuracies.

Dispute any incorrect information immediately.

Common Credit Score Myths

Myth 1: Checking Your Score Hurts It

False.

Personal credit checks do not lower your score.

Myth 2: Income Determines Your Credit Score

False.

Income is not directly included in credit score calculations.

Myth 3: You Need Debt to Build Credit

Partially true.

Responsible use of credit products can help build a positive credit history.

Myth 4: Closing Credit Cards Always Helps

Not necessarily.

Closing older accounts may reduce your average account age.

How Long Does It Take to Improve a Credit Score?

Improvement timelines vary depending on your circumstances.

Minor improvements may appear within a few months.

Significant improvements can take six months to several years.

Consistency is the key factor.

Good Financial Habits That Support a Strong Credit Score

Building a good credit score requires long-term discipline.

Recommended habits include:

- Paying bills on time

- Staying within budget

- Avoiding unnecessary debt

- Monitoring credit reports

- Maintaining low credit utilization

- Creating an emergency fund

These habits contribute to overall financial health.

Frequently Asked Questions

What is a good credit score in the UK?

A good credit score depends on the credit reference agency, but generally falls within the “Good” or higher category.

Is 700 a good credit score in the UK?

It depends on the scoring model. For some agencies, 700 may be considered very good.

Can I get a credit card with a fair credit score?

Yes. Many lenders offer credit-building cards for individuals with fair credit.

How often should I check my credit score?

Monthly monitoring is generally recommended.

Does paying off debt improve credit scores?

Yes. Lower debt levels often contribute positively to your credit profile.

Conclusion

Understanding What is a Good Credit Score in the UK is essential for making informed financial decisions. While each credit reference agency uses different scoring systems, achieving a good or excellent rating can improve your chances of obtaining loans, mortgages, and credit cards on favorable terms.

The most effective way to maintain a strong score is to pay bills on time, manage debt responsibly, monitor your credit report regularly, and avoid unnecessary credit applications.

Building a good credit score takes time, but the long-term financial benefits make the effort worthwhile. By following the strategies outlined in this guide, you can strengthen your credit profile and improve your financial future.