Table of Contents

Introduction

Your credit score is one of the most important numbers in your financial life. Whether you’re applying for a mortgage, personal loan, credit card, car finance agreement, or even a mobile phone contract, lenders use your credit profile to assess risk.

Thank you for reading this post, don't forget to subscribe!Unfortunately, many people make common Credit Score Mistakes without realizing the long-term consequences. A poor credit score can result in higher interest rates, rejected applications, lower borrowing limits, and even difficulties renting a property.

The difference between a good and poor credit score can easily cost you thousands of pounds over your lifetime.

In this guide, we’ll explore the most expensive Credit Score Mistakes, explain why they happen, and show you how to avoid them.

Why Your Credit Score Matters

Before discussing the biggest Credit Score Mistakes, it’s important to understand why your credit score matters.

Lenders use your credit history to determine:

- Whether to approve your application

- What interest rate to offer

- Your borrowing limit

- Loan repayment terms

A strong credit profile can save you thousands through lower borrowing costs.

For additional guidance on credit scores, visit:

https://www.moneyhelper.org.uk

Mistake #1: Missing Payments

One of the most damaging Credit Score Mistakes is failing to make payments on time.

This includes:

- Credit card payments

- Loan repayments

- Utility bills

- Mobile phone contracts

Even one missed payment can negatively impact your credit profile.

Late payments may remain visible on your credit report for years.

How to Avoid It

- Set up direct debits

- Use payment reminders

- Maintain sufficient account balances

- Review statements regularly

Paying on time consistently is one of the fastest ways to build a stronger credit history.

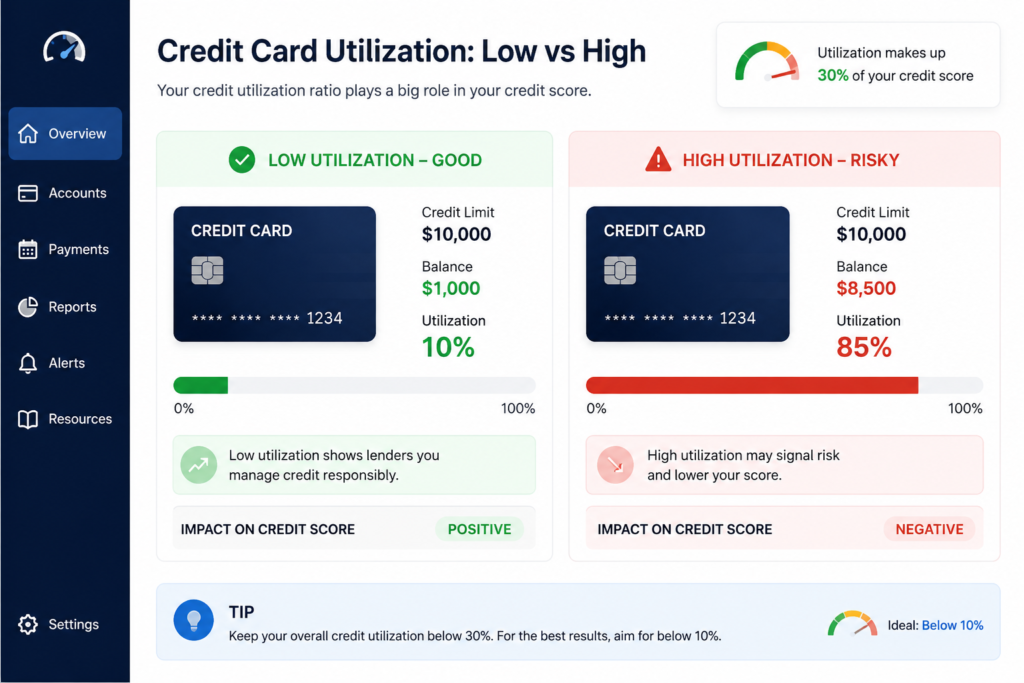

Mistake #2: Using Too Much Available Credit

Credit utilization measures how much of your available credit you’re using.

For example:

If you have a £5,000 credit limit and use £4,500, your utilization is 90%.

High utilization signals potential financial stress to lenders.

This is one of the most common Credit Score Mistakes people make.

Recommended Utilization

Many experts recommend keeping credit utilization below 30%.

Lower utilization often leads to better credit outcomes.

Example

- Credit Limit: £10,000

- Recommended Usage: Under £3,000

Mistake #3: Applying for Too Many Credit Products

Every time you apply for credit, a lender may perform a hard search.

Multiple applications within a short period can make lenders concerned.

Common examples include:

- Credit cards

- Personal loans

- Car finance

- Buy-now-pay-later products

Too many applications may temporarily lower your credit score.

Better Approach

Before applying:

- Check eligibility tools

- Compare lenders carefully

- Apply only when necessary

Avoid making several applications during the same month.

Mistake #4: Ignoring Your Credit Report

Many consumers never review their credit reports.

This can be costly because errors occasionally occur.

Potential issues include:

- Incorrect addresses

- Duplicate accounts

- Fraudulent activity

- Incorrect payment history

One of the most overlooked Credit Score Mistakes is assuming your report is always accurate.

How to Check Your Report

You can review your credit file through:

- Experian

- Equifax

- TransUnion

Regular monitoring helps identify issues early.

Mistake #5: Closing Old Credit Accounts

Many people believe closing older credit cards automatically improves their credit profile.

In reality, older accounts often strengthen your credit history.

Credit scoring models may consider:

- Average account age

- Length of credit history

- Long-term account management

Closing old accounts may reduce your average credit history length.

This is another expensive Credit Score Mistakes that many consumers make.

When Closing an Account Makes Sense

Consider closure only if:

- Annual fees are excessive

- The card encourages overspending

- You no longer need the account

Otherwise, keeping older accounts open can sometimes benefit your score.

Mistake #6: Not Registering on the Electoral Roll

Many UK residents underestimate the importance of electoral roll registration.

Lenders use electoral roll information to verify:

- Identity

- Address history

- Residency status

Failure to register may negatively affect approval chances.

Why It Matters

Electoral roll registration:

- Strengthens identity verification

- Supports credit applications

- Improves lender confidence

This simple step can have a meaningful impact on your credit profile.

Mistake #7: Co-Signing or Joint Financial Agreements Without Understanding the Risks

Joint financial agreements create shared responsibility.

Examples include:

- Joint bank accounts

- Joint loans

- Mortgages

If the other person misses payments, your credit profile may also be affected.

This is among the most expensive Credit Score Mistakes because the consequences can extend far beyond your own financial decisions.

Before Agreeing

Ask yourself:

- Can the other person manage debt responsibly?

- Do I understand the risks?

- Am I comfortable sharing financial responsibility?

Always evaluate carefully before entering joint agreements.

How Poor Credit Scores Can Cost You Thousands

Many people underestimate the true financial cost of a poor credit profile.

Higher Loan Interest Rates

A lower score may result in:

- Higher monthly payments

- Increased borrowing costs

- Less favorable loan terms

Mortgage Costs

Even a small interest rate difference on a mortgage can cost thousands over time.

Reduced Credit Card Offers

Premium rewards cards often require stronger credit histories.

Insurance Pricing

Some providers may use financial information during underwriting decisions.

These hidden costs make avoiding Credit Score Mistakes extremely important.

How to Improve Your Credit Score

If you’ve made some of these Credit Score Mistakes, don’t worry.

Most credit issues can be improved over time.

Pay Every Bill on Time

Payment history remains one of the strongest scoring factors.

Reduce Outstanding Debt

Lower balances improve utilization rates.

Register on the Electoral Roll

A quick improvement step for many UK consumers.

Monitor Your Credit Reports

Check regularly for errors and suspicious activity.

Avoid Excessive Applications

Space out credit applications whenever possible.

Maintain Older Accounts

Long-term account history may strengthen your profile.

Good Credit Habits for Long-Term Success

Building excellent credit is about consistency.

Develop these habits:

- Track expenses monthly

- Maintain emergency savings

- Avoid unnecessary borrowing

- Pay balances in full whenever possible

- Review financial goals regularly

Strong habits reduce the likelihood of future Credit Score Mistakes.

Frequently Asked Questions

What Is the Biggest Credit Score Mistake?

Missing payments is generally considered one of the most damaging credit score mistakes.

How Long Do Credit Score Mistakes Affect Your Report?

Certain negative information may remain visible for several years depending on the type of event.

Can I Improve My Credit Score Quickly?

Some improvements can occur within months through responsible credit management.

Does Checking My Own Credit Score Hurt It?

No. Checking your own report is typically considered a soft search.

Helpful Resources

For additional information:

MoneyHelper UK:

https://www.moneyhelper.org.uk

Experian UK:

https://www.experian.co.uk

Financial Conduct Authority:

https://www.fca.org.uk

Related Articles

You should internally link this article to:

- What Is a Good Credit Score in the UK?

- Best Cashback Credit Cards in the UK for 2026

- Personal Finance for Beginners UK

- How to Build an Emergency Fund from Scratch

- Stocks vs ETFs: Which Investment Is Better?

Final Thoughts

Your credit score affects far more than most people realize. From mortgage approvals to loan interest rates, a healthy credit profile can save substantial amounts of money over time.

By avoiding these common Credit Score Mistakes, you can improve your financial opportunities, increase approval chances, and potentially save thousands of pounds throughout your lifetime.

The good news is that credit improvement is usually achievable through consistent, responsible financial habits.

Start by reviewing your credit report today, correcting any issues, and implementing the strategies discussed in this guide.

Conclusion

Understanding and avoiding common Credit Score Mistakes is one of the smartest financial decisions you can make.

Whether you’re planning to apply for a mortgage, credit card, or personal loan, maintaining a strong credit profile can unlock better financial opportunities and lower borrowing costs.

Take action now, build healthier credit habits, and protect your financial future.Focus Keyword: Credit Score Mistakes

Slug: credit-score-mistakes-that-could-cost-you-thousands

Meta Description:

Discover the 7 biggest credit score mistakes that could cost you thousands in higher interest rates, loan rejections, and financial stress. Learn how to improve your credit score in the UK.

7 Credit Score Mistakes That Could Cost You Thousands in the UK (2026 Guide)

Focus Keyword: Credit Score Mistakes

Featured Image Alt Text: Credit Score Mistakes UK

Introduction

Your credit score is one of the most important numbers in your financial life. Whether you’re applying for a mortgage, personal loan, credit card, car finance agreement, or even a mobile phone contract, lenders use your credit profile to assess risk.

Unfortunately, many people make common Credit Score Mistakes without realizing the long-term consequences. A poor credit score can result in higher interest rates, rejected applications, lower borrowing limits, and even difficulties renting a property.

The difference between a good and poor credit score can easily cost you thousands of pounds over your lifetime.

In this guide, we’ll explore the most expensive Credit Score Mistakes, explain why they happen, and show you how to avoid them.

Why Your Credit Score Matters

Before discussing the biggest Credit Score Mistakes, it’s important to understand why your credit score matters.

Lenders use your credit history to determine:

- Whether to approve your application

- What interest rate to offer

- Your borrowing limit

- Loan repayment terms

A strong credit profile can save you thousands through lower borrowing costs.

For additional guidance on credit scores, visit:

https://www.moneyhelper.org.uk

Mistake #1: Missing Payments

One of the most damaging Credit Score Mistakes is failing to make payments on time.

This includes:

- Credit card payments

- Loan repayments

- Utility bills

- Mobile phone contracts

Even one missed payment can negatively impact your credit profile.

Late payments may remain visible on your credit report for years.

How to Avoid It

- Set up direct debits

- Use payment reminders

- Maintain sufficient account balances

- Review statements regularly

Paying on time consistently is one of the fastest ways to build a stronger credit history.

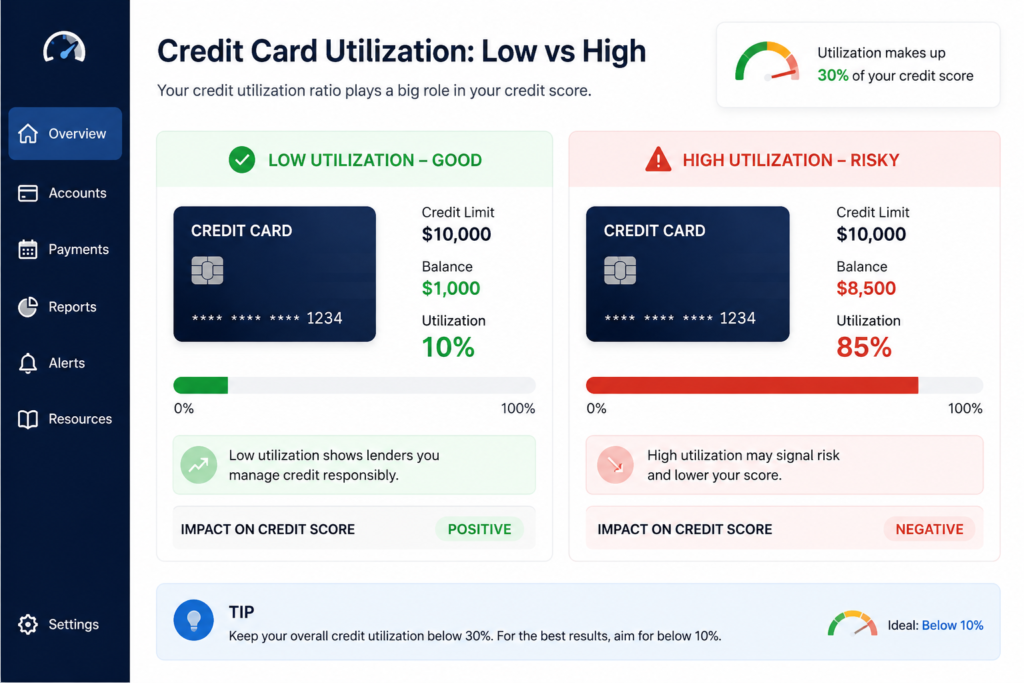

Mistake #2: Using Too Much Available Credit

Credit utilization measures how much of your available credit you’re using.

For example:

If you have a £5,000 credit limit and use £4,500, your utilization is 90%.

High utilization signals potential financial stress to lenders.

This is one of the most common Credit Score Mistakes people make.

Recommended Utilization

Many experts recommend keeping credit utilization below 30%.

Lower utilization often leads to better credit outcomes.

Example

- Credit Limit: £10,000

- Recommended Usage: Under £3,000

Mistake #3: Applying for Too Many Credit Products

Every time you apply for credit, a lender may perform a hard search.

Multiple applications within a short period can make lenders concerned.

Common examples include:

- Credit cards

- Personal loans

- Car finance

- Buy-now-pay-later products

Too many applications may temporarily lower your credit score.

Better Approach

Before applying:

- Check eligibility tools

- Compare lenders carefully

- Apply only when necessary

Avoid making several applications during the same month.

Mistake #4: Ignoring Your Credit Report

Many consumers never review their credit reports.

This can be costly because errors occasionally occur.

Potential issues include:

- Incorrect addresses

- Duplicate accounts

- Fraudulent activity

- Incorrect payment history

One of the most overlooked Credit Score Mistakes is assuming your report is always accurate.

How to Check Your Report

You can review your credit file through:

- Experian

- Equifax

- TransUnion

Regular monitoring helps identify issues early.

Mistake #5: Closing Old Credit Accounts

Many people believe closing older credit cards automatically improves their credit profile.

In reality, older accounts often strengthen your credit history.

Credit scoring models may consider:

- Average account age

- Length of credit history

- Long-term account management

Closing old accounts may reduce your average credit history length.

This is another expensive Credit Score Mistakes that many consumers make.

When Closing an Account Makes Sense

Consider closure only if:

- Annual fees are excessive

- The card encourages overspending

- You no longer need the account

Otherwise, keeping older accounts open can sometimes benefit your score.

Mistake #6: Not Registering on the Electoral Roll

Many UK residents underestimate the importance of electoral roll registration.

Lenders use electoral roll information to verify:

- Identity

- Address history

- Residency status

Failure to register may negatively affect approval chances.

Why It Matters

Electoral roll registration:

- Strengthens identity verification

- Supports credit applications

- Improves lender confidence

This simple step can have a meaningful impact on your credit profile.

Mistake #7: Co-Signing or Joint Financial Agreements Without Understanding the Risks

Joint financial agreements create shared responsibility.

Examples include:

- Joint bank accounts

- Joint loans

- Mortgages

If the other person misses payments, your credit profile may also be affected.

This is among the most expensive Credit Score Mistakes because the consequences can extend far beyond your own financial decisions.

Before Agreeing

Ask yourself:

- Can the other person manage debt responsibly?

- Do I understand the risks?

- Am I comfortable sharing financial responsibility?

Always evaluate carefully before entering joint agreements.

How Poor Credit Scores Can Cost You Thousands

Many people underestimate the true financial cost of a poor credit profile.

Higher Loan Interest Rates

A lower score may result in:

- Higher monthly payments

- Increased borrowing costs

- Less favorable loan terms

Mortgage Costs

Even a small interest rate difference on a mortgage can cost thousands over time.

Reduced Credit Card Offers

Premium rewards cards often require stronger credit histories.

Insurance Pricing

Some providers may use financial information during underwriting decisions.

These hidden costs make avoiding Credit Score Mistakes extremely important.

How to Improve Your Credit Score

If you’ve made some of these Credit Score Mistakes, don’t worry.

Most credit issues can be improved over time.

Pay Every Bill on Time

Payment history remains one of the strongest scoring factors.

Reduce Outstanding Debt

Lower balances improve utilization rates.

Register on the Electoral Roll

A quick improvement step for many UK consumers.

Monitor Your Credit Reports

Check regularly for errors and suspicious activity.

Avoid Excessive Applications

Space out credit applications whenever possible.

Maintain Older Accounts

Long-term account history may strengthen your profile.

Good Credit Habits for Long-Term Success

Building excellent credit is about consistency.

Develop these habits:

- Track expenses monthly

- Maintain emergency savings

- Avoid unnecessary borrowing

- Pay balances in full whenever possible

- Review financial goals regularly

Strong habits reduce the likelihood of future Credit Score Mistakes.

Frequently Asked Questions

What Is the Biggest Credit Score Mistake?

Missing payments is generally considered one of the most damaging credit score mistakes.

How Long Do Credit Score Mistakes Affect Your Report?

Certain negative information may remain visible for several years depending on the type of event.

Can I Improve My Credit Score Quickly?

Some improvements can occur within months through responsible credit management.

Does Checking My Own Credit Score Hurt It?

No. Checking your own report is typically considered a soft search.

Helpful Resources

For additional information:

MoneyHelper UK:

https://www.moneyhelper.org.uk

Experian UK:

https://www.experian.co.uk

Financial Conduct Authority:

https://www.fca.org.uk

Related Articles

You should internally link this article to:

- What Is a Good Credit Score in the UK?

- Best Cashback Credit Cards in the UK for 2026

- Personal Finance for Beginners UK

- How to Build an Emergency Fund from Scratch

- Stocks vs ETFs: Which Investment Is Better?

Final Thoughts

Your credit score affects far more than most people realize. From mortgage approvals to loan interest rates, a healthy credit profile can save substantial amounts of money over time.

By avoiding these common Credit Score Mistakes, you can improve your financial opportunities, increase approval chances, and potentially save thousands of pounds throughout your lifetime.

The good news is that credit improvement is usually achievable through consistent, responsible financial habits.

Start by reviewing your credit report today, correcting any issues, and implementing the strategies discussed in this guide.

Conclusion

Understanding and avoiding common Credit Score Mistakes is one of the smartest financial decisions you can make.

Whether you’re planning to apply for a mortgage, credit card, or personal loan, maintaining a strong credit profile can unlock better financial opportunities and lower borrowing costs.

Take action now, build healthier credit habits, and protect your financial future.